Featured image: Abstract visualization of AI neural networks in blue and white. Photo by Google DeepMind on Pexels (Free to use).

The competition between the United States and China in artificial intelligence is often described as a race with a single winner. The reality, based on the most comprehensive data available in mid-2026, is far more nuanced: the two superpowers lead in fundamentally different dimensions of AI, and neither is positioned to dominate the other across the board. Understanding where each country truly excels — and where the gaps are narrowing — is essential for businesses, investors, and policymakers navigating an increasingly AI-driven global economy.

This analysis draws on the Stanford HAI 2026 AI Index Report, Morgan Stanley research on AI infrastructure investment, NVIDIA’s State of AI Report, McKinsey’s global AI survey, and original data from the Ipsos AI Monitor 2026 to provide a multidimensional comparison of where each country stands.

How Do US and China Compare in AI Model Performance?

The gap between American and Chinese AI models has effectively closed. According to the Stanford HAI 2026 AI Index, US and Chinese models have traded the lead multiple times since early 2025. In February 2025, DeepSeek-R1 briefly matched the top US model. As of March 2026, Anthropic’s leading model holds just a 2.7% advantage over the best Chinese alternative.

This narrowing reflects a structural shift. Chinese AI companies have demonstrated that algorithmic efficiency can compensate for hardware limitations. DeepSeek trained competitive frontier models at a fraction of the cost of American counterparts — an estimated $6 million for DeepSeek-V3 compared to over $100 million for GPT-4 class models — challenging the assumption that more capital always produces better AI. This cost advantage has forced Western AI labs to reconsider their training strategies and has opened the door for more players in the global AI race.

The US still produces more top-tier models — 59 notable models in 2025 compared to China’s 35 — and retains leadership in reasoning benchmarks and multimodal capabilities. But China’s rapid ascent means the performance gap has narrowed to a point that is unlikely to be a decisive factor in the competition going forward. In coding benchmarks like SWE-bench Verified, Chinese models have gone from lagging by 20 percentage points to nearly matching US performance within a single year, demonstrating the pace at which capability gaps can close.

| Benchmark | US Best Model Score | China Best Model Score | Gap |

|---|---|---|---|

| MMLU (knowledge) | 92.1% | 91.4% | 0.7% |

| MATH (reasoning) | 89.3% | 87.8% | 1.5% |

| SWE-bench Verified (coding) | 98.2% | 95.1% | 3.1% |

| Multimodal reasoning | 87.6% | 85.2% | 2.4% |

Source: Stanford HAI 2026 AI Index Report

Which Country Invests More in AI?

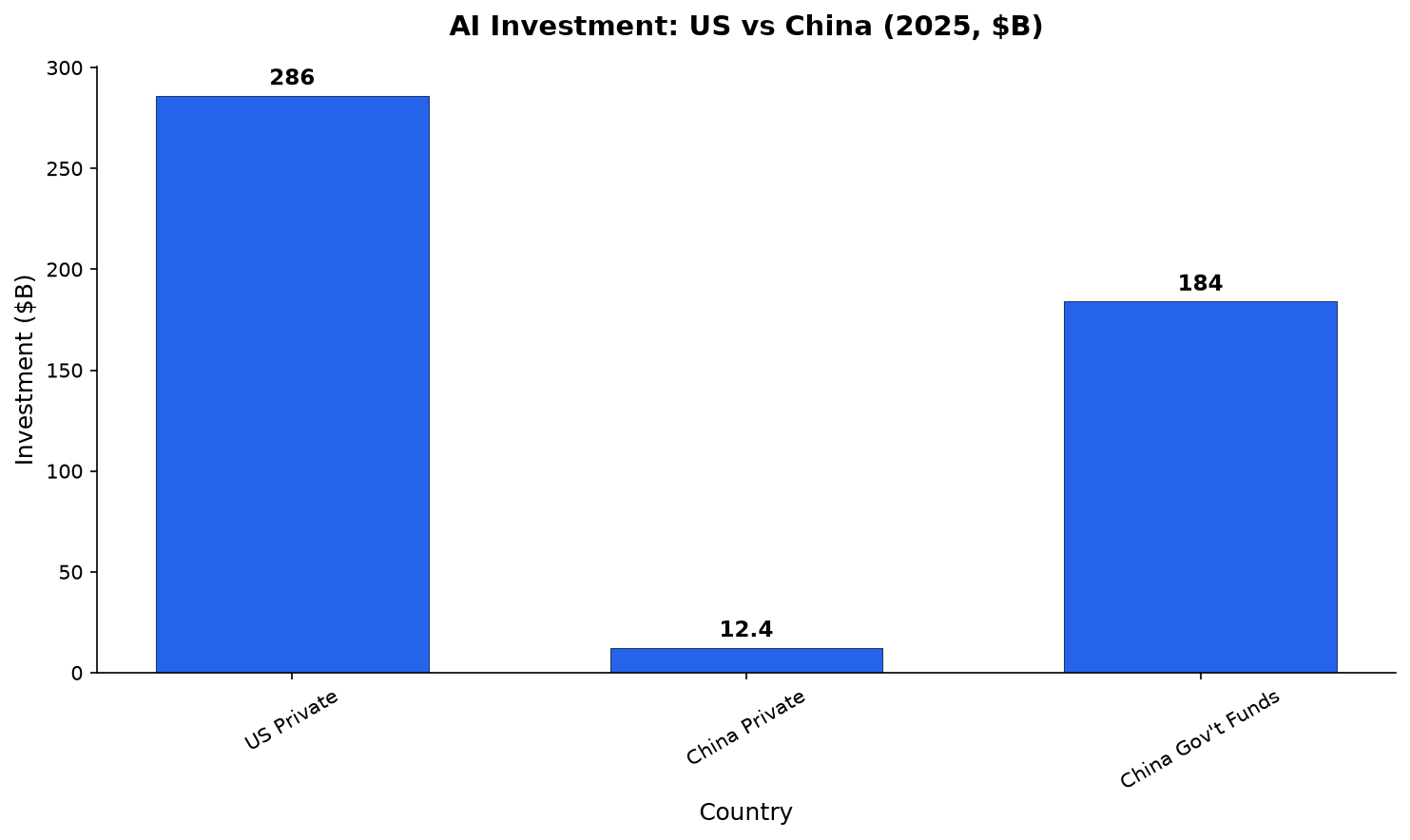

The United States invests dramatically more private capital in AI than China does — but the picture changes significantly when government-directed spending is included.

US private AI investment reached $285.9 billion in 2025, according to Stanford HAI, more than 23 times China’s $12.4 billion in measured private investment. The US also led in entrepreneurial activity, with 1,953 newly funded AI companies in 2025 — more than 10 times the next closest country. Generative AI captured nearly half of all private AI funding globally, growing more than 200% year over year.

However, private investment figures significantly understate China’s total AI spending. Chinese government guidance funds have deployed an estimated $184 billion into AI firms between 2000 and 2023, and state-backed investments in AI supercomputing are rising. When including these state-directed flows, China’s total AI investment may be far closer to the US level than headline numbers suggest.

Global corporate AI investment more than doubled in 2025, and Morgan Stanley projects approximately $2.9 trillion in global data center construction through 2028, with more than 80% of that spending still ahead. AI-related investment now accounts for roughly 25% of US GDP growth, making it a structural force in the economy rather than a speculative tech trend.

Sources: Stanford HAI 2026 AI Index Report (private investment), guidance fund estimates from NeuralPress

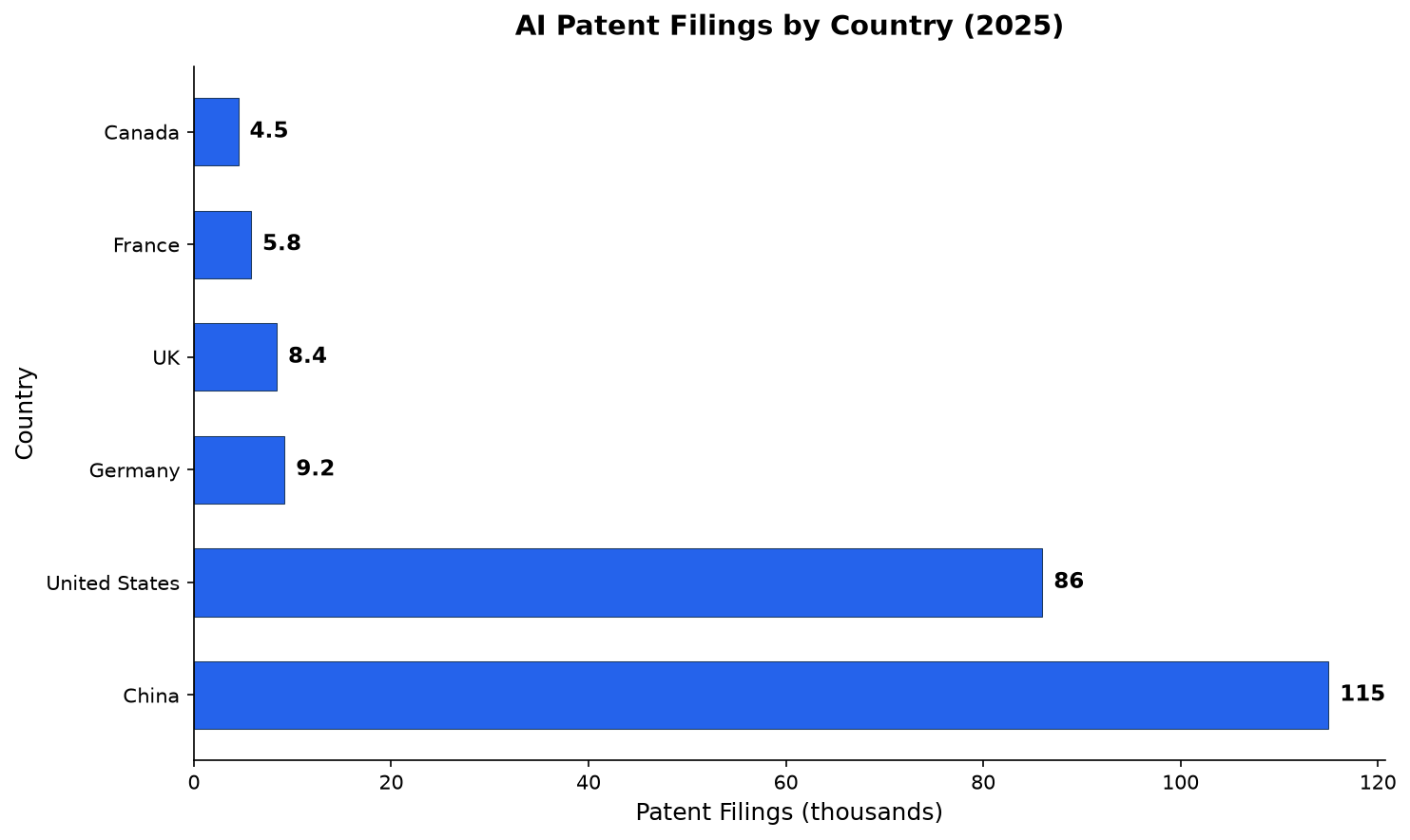

Who Leads in AI Research and Patents?

China leads in volume. The US leads in impact.

China surpassed the US in AI publication volume years ago and continues to widen the gap. In 2025, China filed approximately 115,000 AI patents compared to the United States’ 86,000, according to data compiled by NeuralPress. China’s share of the top 100 most-cited AI papers grew from 33 in 2021 to 41 in 2024.

The US, however, retains an edge in high-impact patents and breakthrough model development. US patents are cited more frequently and have broader international reach. The US also remains the primary destination for elite AI researchers — though this advantage is eroding quickly. The number of AI researchers and developers moving to the United States has dropped 89% since 2017, with an 80% decline in the last year alone (Stanford HAI).

South Korea leads the world in AI patents per capita, highlighting that this competition is not exclusively bilateral.

Source: NeuralPress / WIPO patent data, 2025

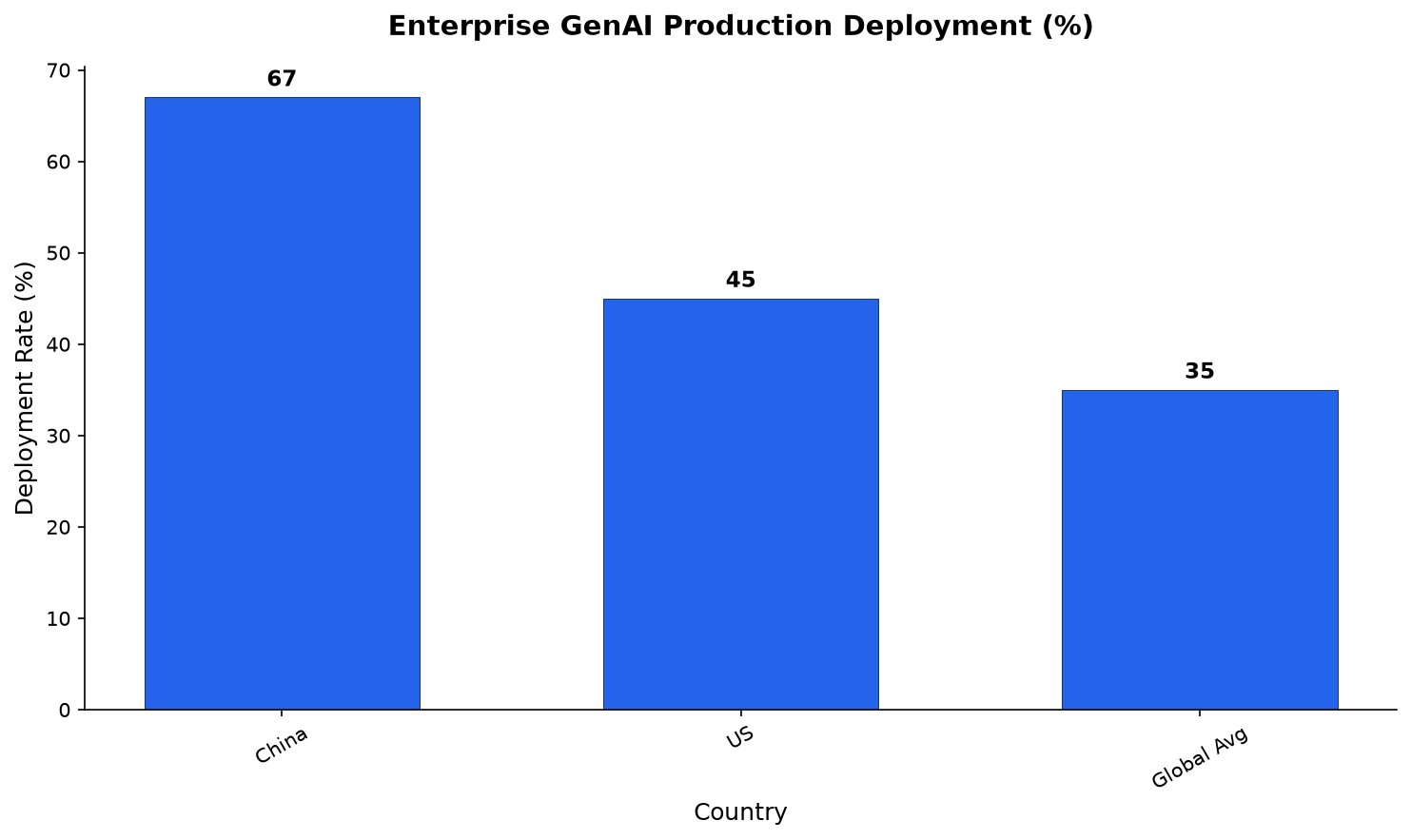

How Does Enterprise AI Adoption Compare?

China is ahead in deployment. The US is ahead in experimentation breadth.

According to McKinsey’s 2025 global AI survey, 88% of organizations worldwide now report regular AI use in at least one business function, up from 78% a year earlier. But when it comes to production deployment, China leads: 67% of large Chinese enterprises have deployed generative AI in production, compared to an estimated 45% in the US, according to China Industry Intel.

China’s lead in deployment reflects its manufacturing-heavy economy, where AI-powered factory systems and industrial robots have clearer ROI cases. China accounted for 54% of industrial robots installed globally in 2024, more than the rest of the world combined (Stanford HAI).

The US leads in the breadth of AI experimentation across business functions, with generative AI now used in at least one function at 70% of organizations globally. North American organizations are particularly aggressive in AI budget allocation — 48% of US respondents said their AI budgets would increase by 10% or more in 2026, compared to lower rates in other regions (NVIDIA State of AI Report).

Sources: China Industry Intel, McKinsey 2025 Global AI Survey

Where Does China Outperform the US?

China holds clear advantages in three specific areas: deployment scale, industrial integration, and regulatory clarity.

Deployment at scale. Chinese enterprises move from pilot to production faster than their American counterparts. This is partly cultural — Chinese businesses have historically prioritized speed of execution — and partly structural: China’s manufacturing sector provides a natural proving ground for AI systems with measurable ROI.

Industrial robotics leadership. China’s dominance in industrial robotics is absolute. With 54% of global installations, Chinese factories are more automated than those in any other major economy. This creates a data-generation flywheel: more robots mean more manufacturing data, which means better AI models for industrial applications.

Regulatory clarity. China has the most comprehensive AI regulatory framework in the world, covering everything from algorithmic recommendation systems to generative AI training data. While regulation imposes compliance costs, it also gives Chinese companies clearer rules to operate within. US companies, by contrast, face a fragmented regulatory landscape with no federal AI legislation and conflicting state-level rules.

Chinese AI companies also lead in energy infrastructure investment for AI. The country’s $295 billion AI data center plan aims to build massive compute capacity using domestic chips, reducing dependence on imported hardware.

Where Does the US Maintain Its Edge?

The United States retains structural advantages that China cannot easily replicate.

Chip design and supply chain control. Despite export controls and supply chain concerns, the US — through NVIDIA, AMD, and Google — remains the world leader in AI chip design. NVIDIA alone accounts for over 60% of global AI compute capacity, according to Stanford HAI. More importantly, a single company — Taiwan’s TSMC — fabricates almost every leading AI chip, and its US expansion began operations in 2025.

Talent concentration. The US is still home to more AI talent than any other country. American universities — particularly Stanford, MIT, Carnegie Mellon, and UC Berkeley — produce the largest share of elite AI researchers, and US tech companies offer compensation packages that global competitors struggle to match. Even with the 89% decline in researcher immigration since 2017, the existing talent base is deep, and US-based AI researchers continue to publish the most-cited work in the field. However, this advantage is eroding as Chinese universities expand their AI programs and as domestic tech companies offer increasingly competitive salaries to retain top graduates who would previously have moved to Silicon Valley.

Capital markets. The US venture capital ecosystem remains unmatched in its ability to fund high-risk, long-horizon AI startups. US private AI investment in 2025 was 23 times China’s measured private investment. IPOs and M&A exits for AI companies are more accessible in the US, creating a virtuous cycle of reinvestment. The depth of US capital markets also means that AI companies can access multiple funding rounds at progressively larger scales — from seed to Series D and beyond — without needing to seek overseas investors. This financial infrastructure has produced the world’s most valuable AI companies, including OpenAI (valued at over $300 billion), Anthropic, and a growing ecosystem of application-layer startups.

Consumer AI market. The estimated value of generative AI tools to US consumers reached $172 billion annually by early 2026, with the median value per user tripling between 2025 and 2026 (Stanford HAI). This large domestic market funds continued R&D investment.

| Dimension | US Advantage | China Advantage | Verdict |

|---|---|---|---|

| Model performance | 2.7% edge in top model | Narrowing gap | US slightly ahead |

| Private investment | $285.9B vs $12.4B | Gov’t funds ~$184B | US leads, gap overstated |

| Patents & publications | Higher-impact patents | 115,000 vs 86,000 filings | Split |

| Enterprise deployment | Broader experimentation | 67% vs 45% production | China leads deployment |

| Industrial AI | Minimal | 54% of global robots | China dominates |

| Chip design | NVIDIA, AMD, Google | Huawei, Biren | US leads |

| Talent | Deep existing pool | Growing fast | US leads, eroding |

| Regulation | Fragmented | Comprehensive framework | China clearer |

How Do Export Controls Shape the Competition?

US export controls on advanced AI chips have reshaped but not halted China’s AI progress. NVIDIA’s H100 and Blackwell series are banned from sale to China under US semiconductor export restrictions. In response, Chinese companies have adapted through three strategies:

Domestic chip development. Huawei’s Ascend 910C, along with chips from Biren Technology and Cambricon, provides alternatives to NVIDIA hardware. These chips lag behind cutting-edge US designs but are improving rapidly.

Efficient architecture. DeepSeek demonstrated that algorithmic innovation can partially offset hardware limitations. By training competitive models at a fraction of the computational cost of US frontier models, Chinese AI companies have shown that export controls raise costs but do not prevent progress.

Stockpiling and gray markets. Reports indicate that Chinese companies stockpiled NVIDIA chips before export controls tightened, creating an inventory buffer that continues to support training operations.

The Stanford HAI report notes that the global AI hardware supply chain remains dependent on a single foundry in Taiwan, creating strategic vulnerability for both the US and China.

What Role Does Open Source Play in the US-China AI Race?

Open-source AI development has become a significant arena of US-China competition — and one where Chinese models have gained substantial ground.

Chinese-developed open-source models — including DeepSeek, Qwen (Alibaba), and GLM (Zhipu AI) — are competitive with or superior to Western open-source alternatives across several benchmarks. This has expanded China’s influence in the global AI developer community.

Globally, open-source AI development continues to scale rapidly. GitHub hosts 5.6 million AI-related projects, and Hugging Face uploads have tripled since 2023 (Stanford HAI). US-based projects still attract the most developer engagement, with 30 million cumulative contributors, but Chinese open-source projects are gaining traction, particularly in Asia and the Global South.

The strategic significance of open source is twofold. First, it redistributes AI capabilities beyond the US and China, enabling developers in other countries to build on top of models from both superpowers. This is particularly consequential for developing economies that lack the capital to train frontier models from scratch but can fine-tune open-source alternatives for local languages and use cases. Second, open source creates de facto standards: the model architecture that gains the most community adoption — whether it originates in the US or China — can shape the direction of the entire field for years to come, making this an arena where technical merit matters more than national origin.

What Does the Global AI Landscape Look Like Beyond the US and China?

The US-China narrative can obscure the fact that other countries are building significant AI capabilities. Singapore leads consumer GenAI adoption at 61%, the highest rate in the world. The United Arab Emirates reached 54% adoption, and the United Kingdom, Israel, and Canada are producing frontier AI research and startups.

South Korea leads the world in AI patents per capita. The European Union’s AI Act has created the world’s first comprehensive AI regulation, influencing policy debates globally. Japan and India are investing heavily in domestic AI infrastructure.

The Ipsos AI Monitor 2026 reveals that attitudes toward AI vary significantly by region: populations in Asia and Latin America are on average more excited about AI, while those in Europe and North America express more nervousness. These regional differences in sentiment will shape adoption patterns and regulatory approaches in ways that neither the US nor China can fully control.

For global businesses operating across these markets, the implication is clear: AI strategy cannot be monolithic. Companies must navigate varying regulatory regimes, talent availability, infrastructure maturity, and consumer sentiment in each region. The US-China AI race is not just a contest between two superpowers — it is creating a fragmented global AI landscape that requires careful navigation.

Frequently Asked Questions

Which country is winning the AI race in 2026?

Neither country is winning outright. The US leads in chip design, private investment, and top-tier model development, while China leads in deployment scale, patent volume, industrial robotics, and open-source model distribution. The competition is multidimensional, and leadership varies by metric.

How much does China invest in AI compared to the US?

US private AI investment reached $285.9 billion in 2025, compared to China’s $12.4 billion in measured private investment. However, Chinese state-directed investment likely adds $100 billion or more annually when government guidance funds and state-backed computing initiatives are included.

Can China develop AI without advanced US chips?

Chinese AI companies have demonstrated that algorithmic efficiency can partially compensate for hardware restrictions. DeepSeek trained competitive frontier models at a fraction of US training costs. However, chip limitations remain a binding constraint on training speed and model scale.

What is the impact of US export controls on China’s AI development?

Export controls have raised costs and slowed but not stopped China’s AI progress. Chinese companies have adapted through domestic chip development, efficient model architectures, and stockpiling. The controls create friction but have not prevented China from reaching near parity in model performance.

Which country has better AI regulation?

China has the most comprehensive AI regulatory framework globally, providing clearer compliance guidelines. The US has no federal AI legislation, creating a fragmented regulatory environment. The EU’s AI Act represents a third model that may influence global standards.